Year 1 Update

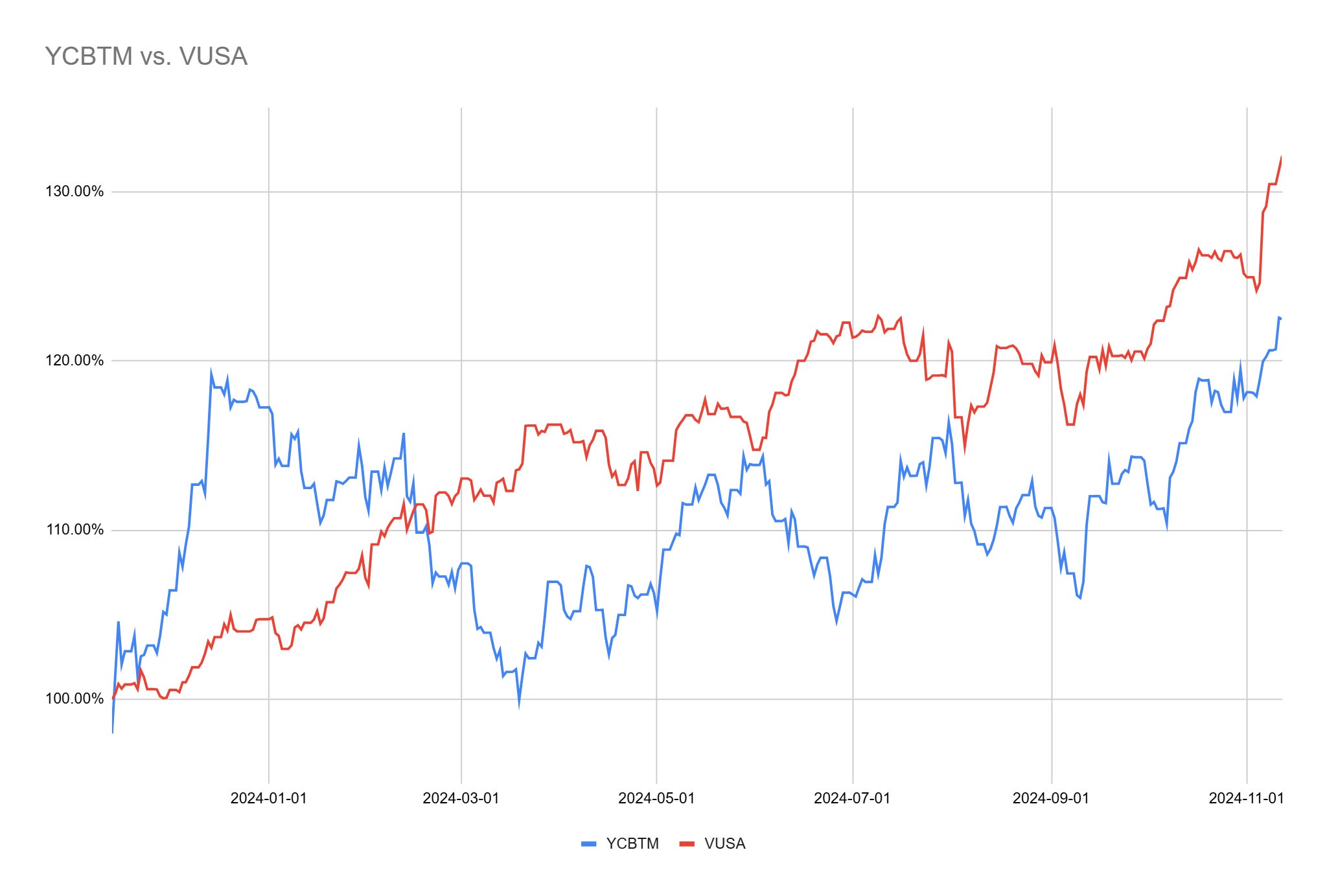

Smashing the FTSE but lagging the S&P

I was off to a good start, but there were some bad prints last Jan/Feb that caused my portfolio to take a prolonged dip while the rest of the market rallied. It happens. Interestingly, GBPUSD is not far off its starting point, so the VUSA is not far off the VUAG at the moment. The currency playing field got levelled by recent sterling weakness.

One year is a very short amount of time in the lifespan of any business or enterprise. I don’t expect to beat the market year in and year out, although it would be nice!

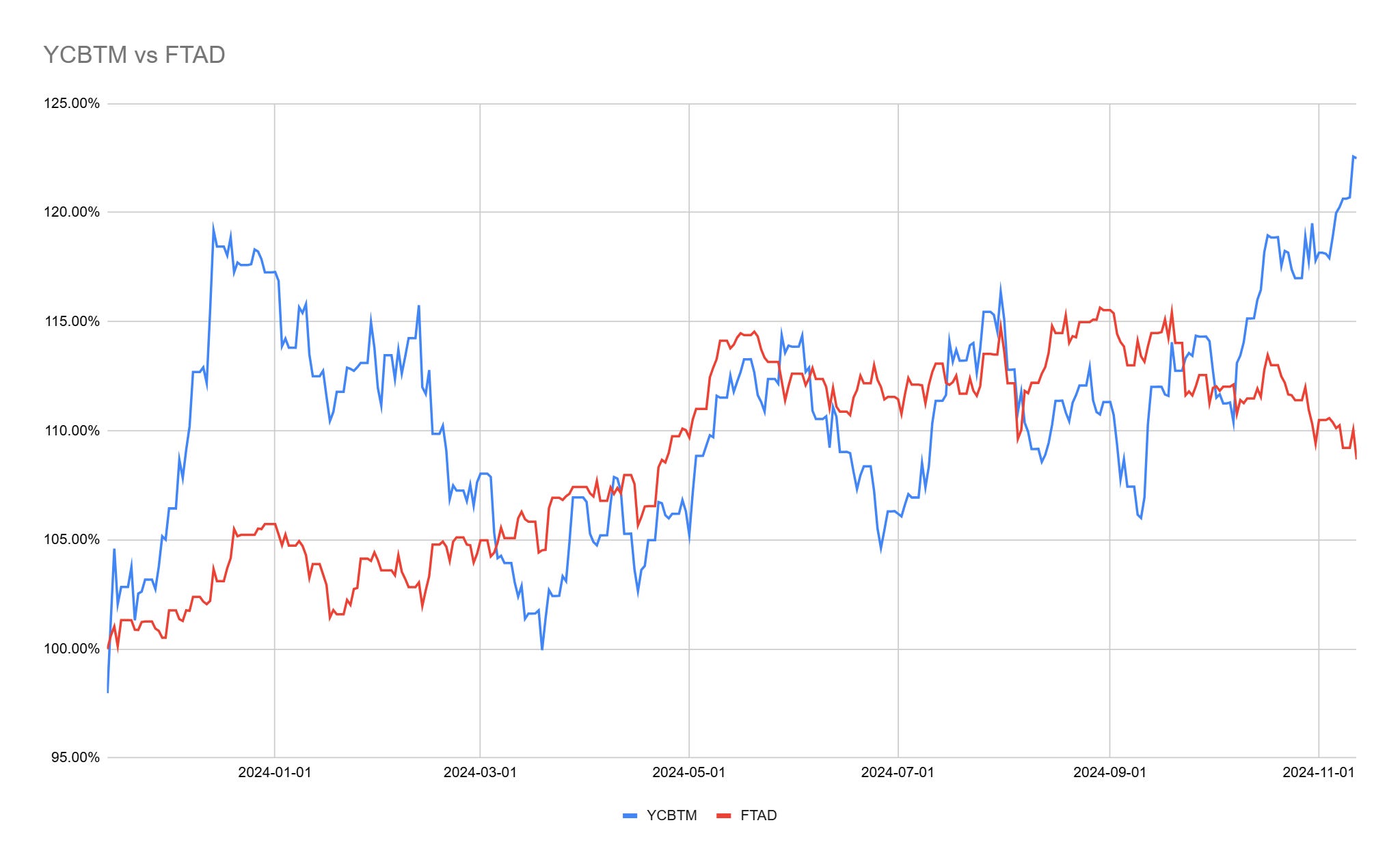

Additionally, I’ve invested a lot of capital outside the US markets, predominantly in the LSE, which is only up around 10% during the same timeframe. Here’s a comparison of YCBTM and the FTSE All Share:

The S&P 500 is becoming increasingly dominated by NASDAQ stocks. 9 of the top 10 stocks by market cap in the S&P 500 are now listed on NASDAQ. Berkshire Hathaway, which is technically a conglomerate and not an individual business, is in 9th position. So there is likely to be an increasingly stronger correlation between tech stock indexes and global market indexes over time. Essentially, index fund investors are now allocating a much larger portion of their holdings to tech, which is also likely to see greater volatility. Index investors tend to shy away from volatility, so I wonder how that will affect their appetite for index funds.

Costs of Trading

I’ve also incurred some trading costs this year.

1.2% to FX losses.

0.99% to fees and charges, mostly due to currency conversion fees.

My currency exchange fees are much higher than a fund. I can’t trade in clips of a size that attract the minimum spread with a wholesale institution. I also pay a very small flat monthly holding fee rather than a percentage of my holdings.

I won’t incur much currency conversion fees in the future as my trading volumes will be significantly lower, but I’m still exposed to currency fluctuations, currently in USD and AUD.

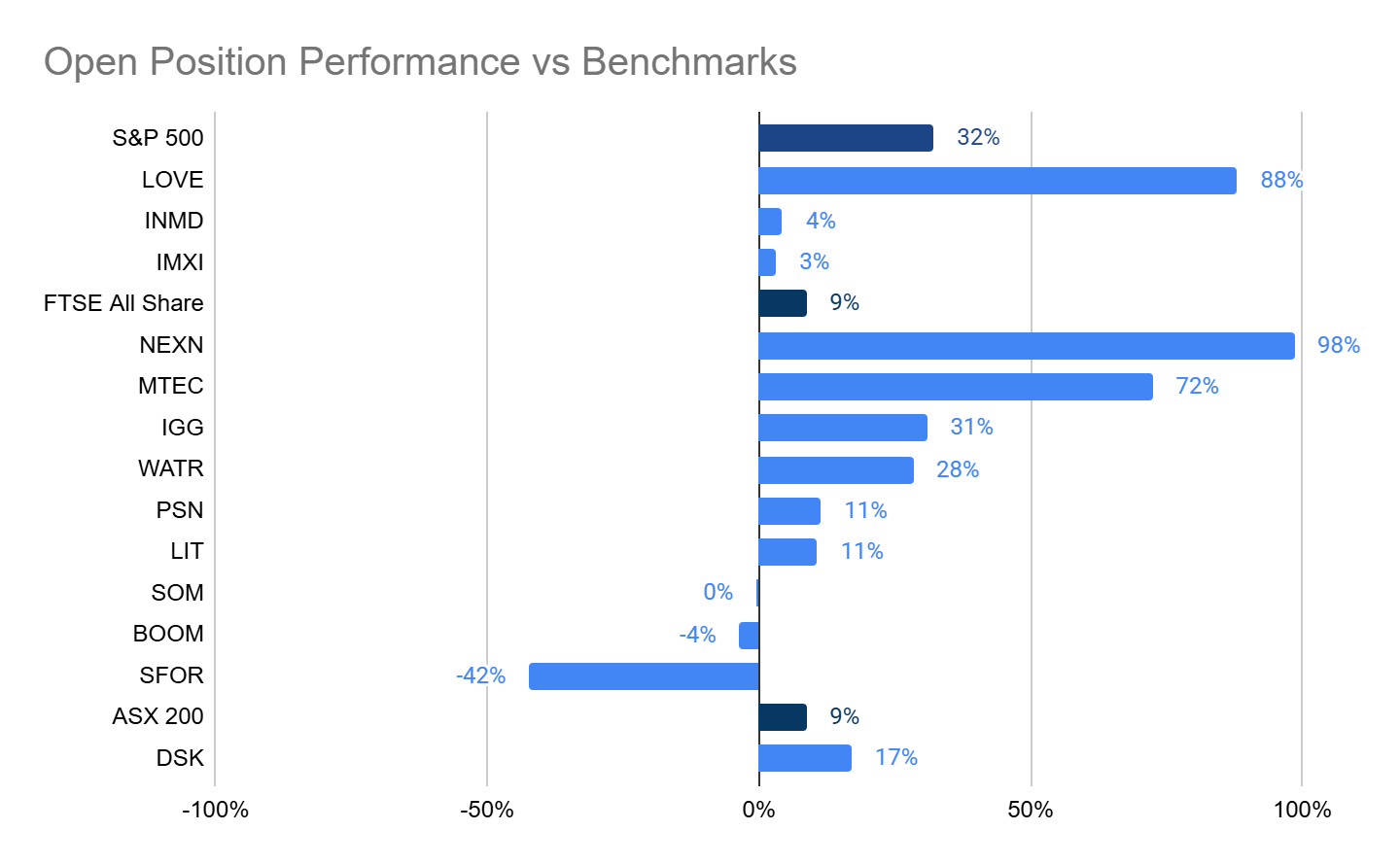

Individual Performance

How has each individual stock performed?

Gain/loss shown above is against the current positions I hold. It doesn’t reflect FX, costs or partial closures. It also doesn’t show previously closed positions, so it doesn’t reflect overall portfolio performance.

In fairness, even with closed positions, I’ve decimated the FTSE All Share. There is still plenty of value in the LSE right now. My US performance has been held back by temporary weakness in InMode and Intermex, so I’m fairly optimistic for the future. Having said that, my significantly oversized Lovesac position meant that overall US performance held up well. My other oversized position was Litigation Capital Management, which was punished by weaker full-year results but still slightly ahead of the all-share.

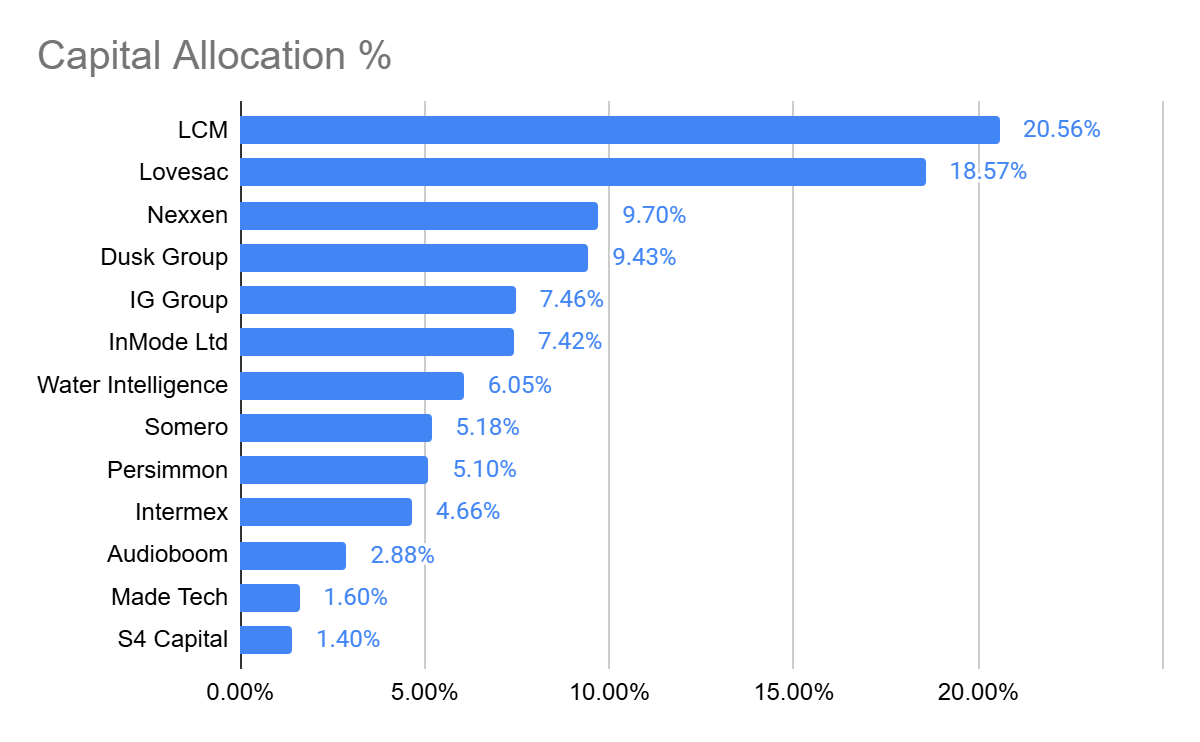

Current Positioning

Here’s a view of the allocation of capital across my holdings:

LCM was by far my biggest original investment. Lovesac has grown significantly and caught LCM up. I expect LCM to outperform Lovesac over time. Nexxen has also performed exceptionally, growing into 3rd position.

I have no intention of altering these allocations any time soon. I’ll let the businesses play out over time. It’s impossible to tell which investments will outperform, so rebalancing in any way is meaningless. If I were to allocate more capital, it would be to LCM first, followed by Inmode.

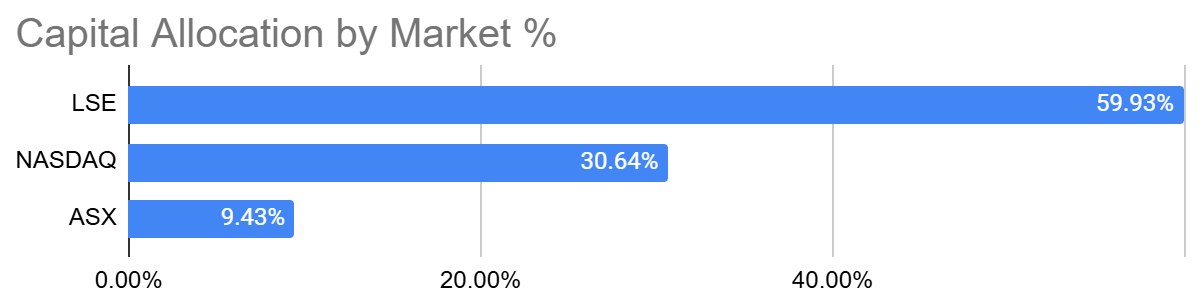

Allocation by market:

How I’ve Changed

Price is only a signal now. I check my stock prices a few times a day, but solely to see what’s up or down. I use that as a signal to investigate; it’s an alert that there might be some news I should be aware of. I’m no longer bothered by big gains or big losses; this is just the market reacting. I’m much more interested in the performance, prospects, and underlying economics of the businesses. As I’ve mentioned before, it’s hard for these to change fundamentally over the course of a couple of quarters or even a couple of years. What drives price in the short term is expectations and speculation. Business fundamentals drive prices over the long term.

I’m very price sensitive. Price is the key to valuation. Growth at any price is not my mantra. Businesses can’t grow 20% a year to infinity, not without violating some competition laws in unregulated markets. I have a 10-year timeframe, and if the price doesn’t make sense based on the business fundamentals and prospects, I’ll take a pass. Maybe I’ll miss the next big thing; I’m ok with that. I don’t want to be at the top of the league; I just want to be above the median.

I’ve also seen the wisdom of concentration. With more time to spend on each individual business, I’m far more learned, which makes me far less prone to short-term overaction. Diversification is not risk management; it’s return dilution. Good risk management comes from the right understanding of the business and markets in which it operates. You can do far more research than some of the large funds. For instance, a multi-billion fund in particular spends on average 1.5 days of analyst time per year on each stock. You can do better than that, especially given 70% of the market is absolute trash that you can quickly skip past.

I also say “right understanding” here, as I don’t need to be an expert in certain areas. For instance, I can’t become a litigation expert, but then I don’t need to be one to understand the economics and prospects of Litigation Capital Management. I don’t need to follow each individual case; it’s the portfolio of litigation over time that matters, and we have good metrics there. I’ll leave the litigation expertise to the barristers!

This point is important, as I see far too many investors spending large amounts of time investigating a current product in depth, like they were doing some Gartner analysis. Then the business or market shifts and goes in a slightly different direction. The ability of a business to exploit its products and innovate, adapt, and adjust is far more important than any single product. Not to mention the ability to defend your margins. The iPhone and iOS have adapted and evolved significantly since their inception; consider the concept itself and dynamics of the business and markets before you spend too much time analysing a static product at a point in time.

I also shy away from the next hot thing. There is far too much competition bidding up the prices in the hope of bagging a windfall. These industries are also capital intensive due to the rapid innovation, with marginal prospects of ever breaking even. They require huge consecutive injections of capital to keep them going. Typically, these businesses have logarithmic potential, but the market seems to assume exponential. Take AI, the next Chat GPT or Gemini is unlikely to provide the same size improvement over the prior version. Too risky for me; I’ll leave these to the VC funds.